- US headline inflation rises to 7.5% YoY, the highest in four decades

While most price distortions will fade over the course of the year, stubbornly high numbers increase the risk of a policy mistake by the Fed.

- Strong US inflation triggers another rise in government bond yields, the 10yr Treasury yield briefly rises above 2% while the curve flattens

Geopolitical developments and investor concerns raise the hurdle for a further rise in yields near term. A pause for digestion now appears warranted.

- Omicron based mobility restrictions cause weak household activity over Lunar New Year

Solid credit data for January and the PBoC’s monetary policy report suggest that policy support will help to boost growth going forward.

Weekly Market Update

Investments

| Article

| 14 Feb 2022

|

Weekly Macro & Markets View

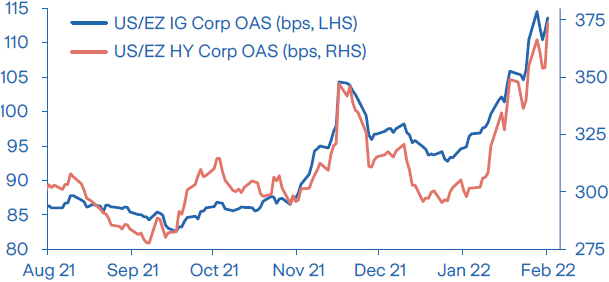

Gap downs seen in credit

Source: Bloomberg, Barclays Indices

Note: Global OAS is 50% US and 50% European Corp Index OAS

Last week was rather rough for risk assets as an upbeat investor mood was shattered mid-week by concerns around inflation, monetary policy and geopolitical developments. Indeed, a higher than expected US CPI reading on Thursday at a 7.5% YoY rate was the highest in four decades. But this didn’t roil markets as much as the opinion from St. Louis Fed President James Bullard that the Fed should raise rates by 100 basis points by July 1, 2022. Furthermore, news that the US expects Russia to imminently invade Ukraine further caused investor sentiment to weaken on Friday.

It has been our fear for a few weeks now that credit markets would be vulnerable to gapping down if equity volatility were to persist. It seems that these fears are coming to fruition, with the price action in credit becoming increasingly volatile over the last couple of weeks. While the US high yield market had the worst YTD start since 2016, BBs had the single biggest one day drop on Friday since 2020. European credit notably underperformed US, with fund flows and primary markets showing notable signs of weakness. However, despite the recent spread widening, credit spreads still seem low in a longer-term context. Consequently, the risk of further gap downs in credit is likely to remain for some time.

US: Inflation rises to the highest in four decades

Headline CPI inflation accelerated to 7.5% YoY while Core CPI rose 6.0% YoY in January. Inflation remains significantly distorted by a number of factors like unusual price increases in used cars, is exacerbated by the rise in energy costs, and helped by base effects as inflation was still very weak a year ago. Most of these effects are expected to work in reverse this year, leading to rapidly falling inflation rates. Nevertheless, some underlying price pressures like rising shelter costs are likely to be stickier and will help to keep core inflation above target for some time to come. Stock markets face some headwind as stubbornly high inflation numbers increase the risk that the Fed will tighten its policy too much in an environment where growth and inflation are already falling. The equity sell-off accelerated on Friday as rising tensions between Russia and Ukraine weigh on investors’ minds. Finally, on a more positive note, the NFIB’s jobs-hard-to-fill measure ticked down to the lowest since last June, indicating that labour market conditions are easing.

Bonds: Treasury yields snap higher on a strong CPI print

Strong US inflation data triggered another rise in Treasury yields, with six rate hikes now fully priced in for 2022. The 2yr yield rose by over 21bps on the CPI release, while the 10yr yield closed above 2% for the first time since mid 2019, before slipping back as tensions around Ukraine rose. The Treasury curve flattened further, with the 2/10 spread at only 40bps, down from 80bps three weeks ago. The longer end of the curve was largely unaffected by the sell-off, with the 5yr5yr forward rate still rangebound around 2%, well below the Fed’s 2.5% guidance. European core yields found some stability as ECB commentary broadly confirmed the hawkish policy tilt in the prior week. Periphery spreads widened further but are not a cause for concern at the current relatively benign levels. Although some further upside to yields is possible, given a backdrop of strong growth and inflation and an improving Covid situation, a pause for digestion appears warranted, and geopolitical tensions could also weigh on yields near term.

Japan: Consumer sentiment takes a hit due to surging Omicron cases

The Bank of Japan’s consumption index suggests that private consumption was strong in Q4 last year. However, we believe that consumption will have experienced a severe hit early this year due to the surging Omicron virus wave. For the first time since Covid broke out, Japan’s new infection cases per capita are higher than those in the US. About half of the country is under a quasi state of emergency as hospitalisation rates increase, even though intensive care units are faring better than during the Delta variant surge. The Eco Watchers Survey household component tumbled a hefty 24 points in January, a drop comparable only to the Covid induced slump in 2020 and the drop after the 2011 tsunami. News is also concerning in the manufacturing space as Toyota announced production cuts due to ongoing chip supply-chain problems. Regular wages were stable in January and overtime payments even solid, but the semi-annual bonus payments were disappointing, and higher CPI inflation hit worker’s real incomes.

China: Soft Lunar New Year activity meets stronger credit growth

Lunar New Year activity was lacklustre in terms of travelling, services consumption, and home buying. Compared to pre-Covid levels, domestic trips were down 26.1%, while tourism revenue shrank 43.7%, slightly weaker than a year ago. The government had requested citizens refrain from travelling. On a positive note, that may be good for manufacturing production as migrant workers are now quickly returning to their factories. Meanwhile, credit data for January were strong, mainly supported by local governments frontloading special bond issuance as well as solid corporate bond, bill and loan growth. Household loan growth remained weak amid still decreasing home sales. Overall, broad credit growth picked up to 10.5% YoY. Reading the just released Q4 monetary policy report by the PBoC suggests to us that more proactive policy easing seems likely, which may even become evident by another policy rate cut this week. However, deleveraging policies will remain intact, as the PBoC makes clear that the property market will not be used to stimulate the economy.

LatAm: Central banks are concerned about the risk of inflation expectations de-anchoring

In Chile, January inflation reached 1.2% MoM, twice the market expectation, and reaching 7.7% YoY, the highest level since November 2008. Inflation continues to be widespread, with core inflation explaining the month's surprise and rising 7.1% YoY. At its next meeting, we expect the central bank will increase the policy rate by 150bps to 7%. In Mexico, January headline inflation was above expectations reaching 0.6% MoM, with the YoY level decreasing from 7.4% to 7.1%. However, core inflation accelerated, reaching 6.2% YoY. Banxico hiked the policy rate 50bps to 6%, as expected, and revised up again its inflation forecast. We expect another 50bps of hike in the next policy meeting. In Brazil, headline inflation is in line with expectations, reaching 10.4%. Core inflation continues to accelerate, reaching 7.9% YoY. The minutes from the last policy meeting had a hawkish tone and were explicit in saying that the monetary tightening process should be more restrictive than that used in the reference scenario throughout the relevant horizon.

What to Watch

- In the US, the latest set of PPI numbers will give important insights into the underlying price pressure while retail sales are expected to recover from the dip in December.

- In the Eurozone, the German ZEW survey and industrial production data for the region as a whole are expected to indicate that the economic recovery remains on track.

- We expect the Philippine central bank (BSP) to remain accommodative by keeping policy rates unchanged. In Australia, we expect slightly weaker labour market data for January. Japan will announce various domestic and foreign trade activity data. In China, the PPI-CPI gap will remain high in January before shrinking in the months to come. Singapore will announce its FY22 budget. Indonesia is expected to show strong export data for January.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.