This site is for financial adviser use only.

Evolving our Total and Permanent Disability offering and pricing

The need to evolve Total and Permanent Disability Insurance

The purpose of both TPD and Income Protection is to replace customers' short and long-term income whilst being able to focus on their health journey and adjust to the changing circumstances they face.

TPD also helps to cover the additional costs our claimants incur because of their disability, which can vary in size depending on the severity of the condition.

This can make all the difference when the rubber hits the road. The resilience of our claimants has been inspiring, and their unique journeys to better health have always been supported collectively by you, us, their support networks and of course their medical professionals.

Please watch a video update from Kieran Forde who details the challenges and opportunities with TPD in an evolving market.

Pricing changes for existing customers

We must continually review our premiums to ensure they fairly reflect the claims experience of that portfolio and reflect the true cost of providing that valuable protection. To ensure the offerings' sustainability, we need to increase the price of our TPD policies and legacy IP policies for existing customers.

What are the changes for existing customers?

Total and Permanent Disability

- Wealth Protection policies written prior to 21 December 2015 will have premiums (variable age-stepped and variable) increase by 20%.

- Wealth Protection policies written between 21 December 2015 and 6 May 2023 will have premiums (variable age-stepped and variable) increase by 25%.

Income protection

- Wealth Protection Income Protection policies written between 21 December 2015 and 26 September 2021 will have premiums (variable age-stepped and variable) increase by 10%.

- Active, FutureWise including SuperProtector Income Protection policies written prior to 26 September 2021 will have premiums (variable age-stepped and variable) increase by 10%.

Death cover

- Wealth Protection death premiums will increase by 5% per year from age 80 onwards.

These increases are in addition to age and CPI increases. These updates will not apply for any policies within their two-year rate lock until the end of the rate lock.

Changes to new business rates

In addition to these changes there will also be a reshape in rates for new business quoted after the 24th of February 2024.

We will be removing the management fee on all Wealth Protection policies quoted after 24th of February 2024.

When will the changes happen?

Changes to premium rates will be effective from 24th of February 2024.

This means that renewal notices going out from this date will include the new higher rates and customers will need to pay the new higher premiums from their first policy anniversary 42 days after 24th of February 2024, or if they make an alteration on their policy after 24th of February 2024.

Get prepared with the February transition rules

If a quote has been produced before 24th of February 2024, this can be honoured for 60 days from the quote date or until renewal (whichever is first).

Policy alteration quote requests before 24th of February 2024, but quote is provided after – New rates will apply.

Resources

Riskinfo round table series

This industry-wide Round Table discussion considers the critical issues associated with the Total and Permanent Disability product currently offered in the Australian market and whether it remains both sustainable and whether it remains both sustainable and fit for purpose.

Watch Zurich TPD Round Table – Part 1

In the second segment of this TPD Round Table series, this diverse and passionate industry panel discusses the challenges associated with how to assess ‘Permanency’ for the purpose of TPD claims, and how subjectivity is ultimately involved in those claims cases where this element is so difficult to determine…

The rise of mental illness-related TPD Claims and the impact this is having on premium pricing for all TPD policy holders is the focus of this next instalment in our TPD Round Table discussion.

In the fourth part of this TPD Round Table video series, your panel of peers makes it clear how important it is for advisers to have the capability to offer their clients options and flexibility when it comes to TPD product solutions – especially in an environment in which premium affordability is close to breaking point for many policy holders…

In the fifth and final instalment of this TPD Round Table discussion, the panel turns its focus towards finding solutions and a future pathway that will enable the Australian TPD offer to remain sustainable, fit for purpose, affordable and accessible for all who would benefit from the critical protection role this product serves…

Future of work knowledge Hub

We have curated global thought leadership for you to read. Please take a look.

Zurich Evolve

Health is a journey that’s always changing. No matter how life evolves for the people we insure, they can count on us to support them every step of the way.

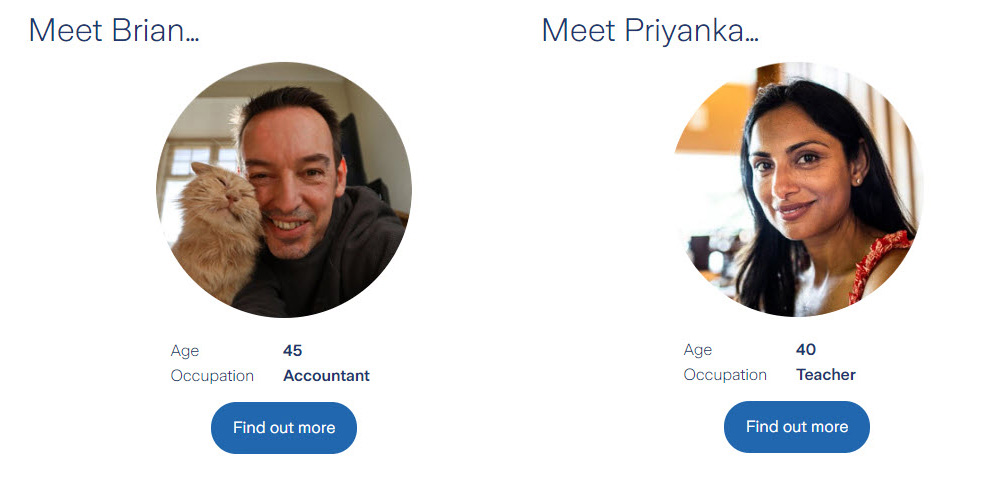

Find out how you can make insurance more affordable

These two customers recognise the value of insurance and understand how vital it is to financial security. However, cost of living pressures are a concern. Explore how they can make insurance more affordable.

Key dates

Changes to premium rates will be effective from 24th of February 2024

This means that renewal notices going out from this date will include the new higher rates and customers will need to pay the new higher premiums from their first policy anniversary 42 days after 24th of February 2024, or if they make an alteration on their policy after 24th of February 2024.

Key dates

Changes to premium rates will be effective from 24th of February 2024

This means that renewal notices going out from this date will include the new higher rates and customers will need to pay the new higher premiums from their first policy anniversary 42 days after 24th of February 2024, or if they make an alteration on their policy after 24th of February 2024.

Download the Cost of care whitepaper

The cost of care whitepaper brings together detailed research across the broad spectrum of injury and disease. The research is designed to help financial advisers better understand the underlying costs that may be incurred and the prevalence of various common illnesses and conditions in Australia today.

Count on us to protect what matters most

In 2022 Zurich Retail life paid more than $390 million in life insurance claims to 2,797 customers, which gives you the confidence that if things go wrong, we will be there.