This site is for financial adviser use only.

February 7 Product Updates

Adviser Information Hub

Everything you need to know about our product changes from 7 February, 2025

We’ve created this ‘Information Hub’ as a one-stop knowledge and resource centre to help you understand the changes we are implementing to our products from 7 February 2025.

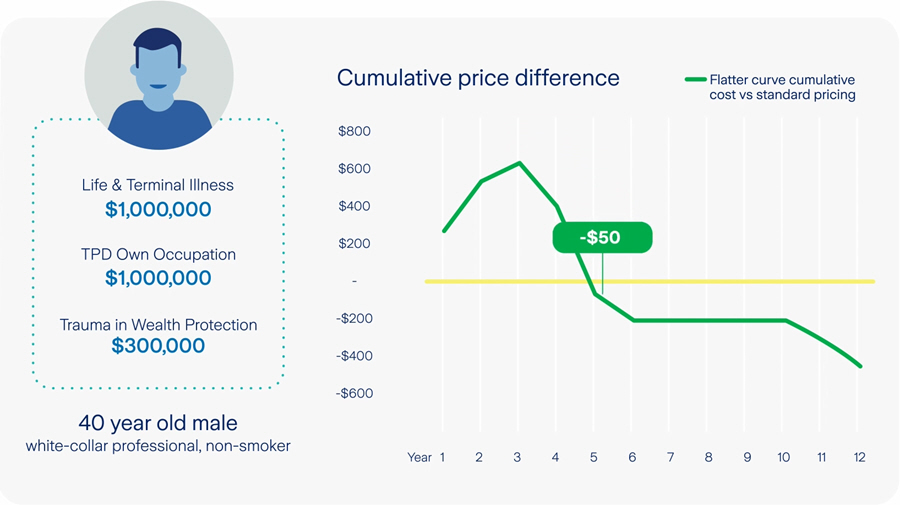

The new pricing options provide more stability and long-term value for your clients and offer more choice when designing solutions to better fit individual circumstances. Our new Zurich pricing option – Flatter Pricing – is available for all Wealth Protection products and Active Income Protection. It’s a slightly higher year 1 price, but can be used to give clients smaller year-on-year increases in premium and a cumulatively lower cost after approximately five years from when the policy starts compared to our standard pricing.

Watch Below: Head of Zurich Propositions, Ioana Logan, explains how this new option provides more consistent pricing throughout the policy lifecycle.

We are also improving our trauma definitions and underwriting requirements which are outlined below.

These changes aim to provide more stability and long-term value for customers and offer more choice and optionality when designing solutions that better fit individual circumstances.

From 10 February 2025 you will now have two pricing options available to you;

| Option | What it is | How it works | Best for |

|---|---|---|---|

| Option 1: Lower Upfront Pricing (Standard) | This option has lower initial year 1 premiums. | The payments start low but will increase more over time. | Clients who want to pay less initially but are accepting of higher payments later in their policy lifecycle. |

| Option 2: Flatter Pricing | This option has higher premiums in the beginning, but the increases are smaller over time. | The payments start at a higher price compared to standard pricing but is more stable and end up being cumulatively cheaper after about five years. | For clients that prefer more predictable payments and are planning to keep the policy for longer than about five years. |

Key points to remember

- Short-term savings vs long term affordability: Flatter pricing starts out higher but becomes cumulatively cheaper after about 5 years.

- Stability: Flatter pricing will remain cumulatively cheaper than standard pricing after approximately 5 years, even if there are future pricing increases. Premiums for both options are not guaranteed and can change. However, we won’t change the "Flatter pricing" option without making the same change to “Standard” pricing.

- No Switching: Once a policy is in force, a customer cannot switch between the pricing options.

For more information – please see our adviser guide (from February 7 2025) for a detailed breakdown of how the new pricing option works.

Updated versions will be available from 7 February 2025: Zurich Wealth Protection PDS I The Adviser Guide

How to quote from 10 February 2025

A new field called "Selection pricing" will appear in Zurich life quotes (accessed through The Adviser Portal), with the two options available in a drop-down menu:

- Lower upfront pricing (standard)

- Flatter pricing

You can easily compare the pricing and projections of both options by duplicating a quote and doing a side-by-side comparison.

If you don’t choose an option, pricing will default to the standard, lower initial pricing.

Two improvements are being made to trauma definitions. These will apply to new policies and are being passed back to customers who have policies with PDS dated 1 October 2024.

| What has changed | The benefit |

| Angioplasty (triple vessel) definition | The definition covers angioplasty of all arteries and their branches |

| Cancer (excluding early-stage cancers) definition | An exclusion for certain thyroid cancers is removed |

Updated versions will be available from 7 February 2025: Zurich Wealth Protection PDS I Zurich Active PDS I The Adviser Guide

After an extensive review with our medical experts, we have simplified our underwriting requirements.

|

What has changed |

The benefit |

|

GP Medical Exams replaced with Express Exams |

Nurse can be arranged at convenient appointment times making it quicker and simpler for the customer to attend. Capture the same key screening elements including BMI, blood pressure and urine test just as effectively. |

| HIV and Hep B& C removed from mandatory requirements |

Removal of blood tests. The incidence of HIV and Hep B & C in the general population in Australia is very low with ongoing advances in medical treatment only expected to further minimise incidence and severity into the future. |

| Breast Exams replaced with Mammograms |

Mammogram is seen as a more favourable customer experience. It also provides a more sophisticated examination technique. |

| Stress ECGs replaced with Stress Echocardiograms |

The echocardiogram is a more effective investigation than the stress ECG, especially in younger individuals. It provides a result from the first appointment which leads to a quicker underwriting decision where incidental cardiac findings are found. |

This applies to: Zurich Wealth Protection and Active

Updated version will be available from 7 February 2025: The Adviser Guide